The ever advancing push of technology is remarkable. The first iPhone only came out in 2007. iPads were even later to join the party, coming out in 2010. In 2009, people were still using Netflix (in Canada) to order DVDs. Things that people once thought were indispensable become relics (hello, Panasonic Shockwave!) and things that people can’t fathom eventually become reality (go, go, Gadget watch phone!).

We’re on the precipice of something similar in the world of investment management. Technological advances are allowing asset managers to rethink how they choose stocks and manage risk. Artificial intelligence isn’t a new concept – the famous IBM Deep Blue beat Gary Kasparov in chess way back in 1996 – but it is always making new advances into new industries. Even in the chess world, AI has changed a lot since 1996. Now, chess AI like StockFish and Google’s AlphaZero compete head to head, each performing hundreds of calculations per second. It should be noted that StockFish, which has been noted to be “well beyond the skill of any grandmaster” was beaten by AlphaZero, an AI that utilizes machine learning to “learn” which moves are best. Our platform – Boosted Insights – operates on a similar machine learning principle, “learning” which equities perform best under different conditions.

All that is to say, it’s an exciting time in the world of new technology, but some fundamental managers may be left wondering how they can actually use AI in their process. Combining a fundamental manager’s capital markets expertise and the vast amount of data available today is called quantamental investing and here, we’ll discuss some of the ways institutional investors can harness artificial intelligence and machine learning for their portfolios.

Risk Mitigation

For many portfolio managers, the question of “How can I reduce risk in my investments” is almost as important as finding alpha. We’ve already discussed how machine learning can be utilized to find and identify risk to mitigate drawdowns, even in black swan events like the quant shock, unique stock movements like GME and world pandemics like Coronavirus. Asset managers can use machine learning to reduce risk by:

- Using AI to identify a targeted short basket as a hedge for their book. AI can find non-intuitive links and use its big data processing capability to highlight stocks that may provide better return than a typical hedge.

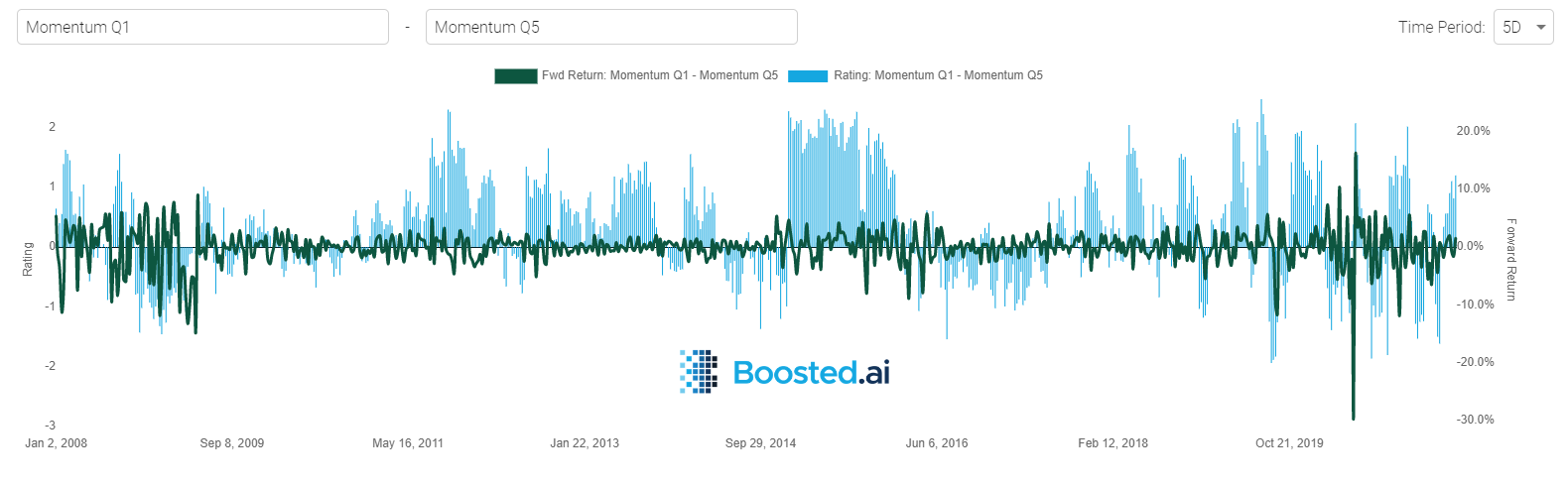

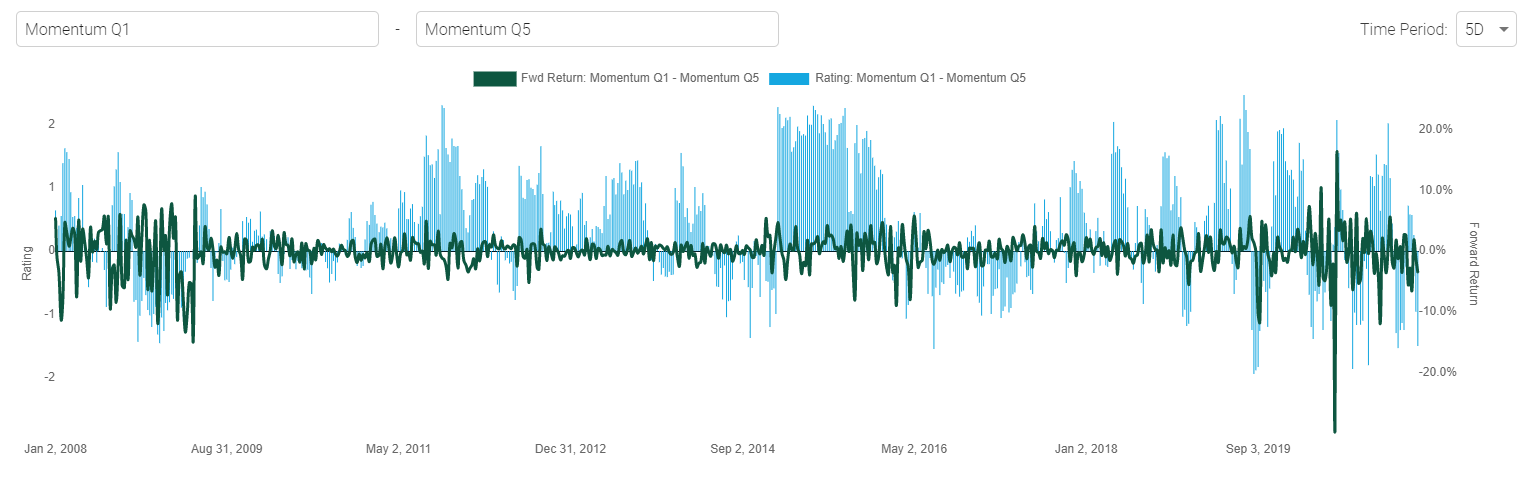

- Giving visibility into all risk factors. Software like our Boosted Insights can give managers better sight into what risk factors are at play and when. Utilizing AI, it can give signals of when regime shifts may be approaching. We discuss this more in our post about factor timing, here.

- Utilising traditional and machine learned risk factors to implement factor timing, where the portfolio manager can look at stocks based on how well machine learning thinks they will do, but also ranked on their risk factors. We show how these unique signals can give investors an early edge in our second post on factor timing, here.

Idea Generation

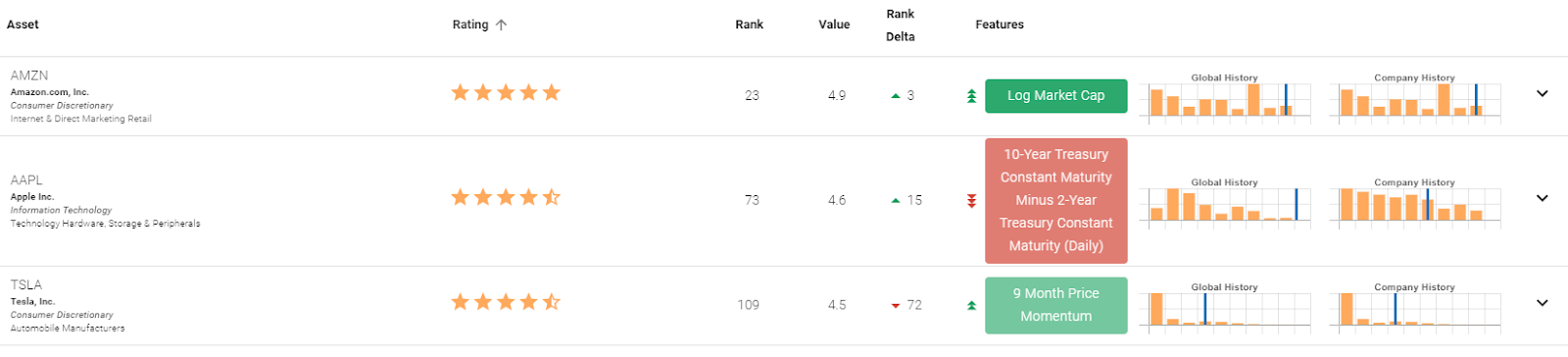

Every fund manager uses data in some way. The more traditional process of looking at P/E ratios, dividend yields and so on, is all based on analyzing available data and making decisions based on the findings. Artificial intelligence for investment is not so different. It is simply able to operate faster and more efficiently than the average human. For example, within our proprietary algorithms, our machine learning compares every stock, on every metric the user inputs, against every other stock and ranks them dynamically. In the S&P 500, that is 250,000 calculations. We certainly wouldn’t want to do that many comparisons manually! Implementing AI within their portfolios can enhance a fundamental manager’s research process by:

- Providing a dynamically updated, ranked list of stocks within the investment manager’s universe, along with full explainability of why the machine likes or dislikes any particular stock.

- Saving them time and effort. The PM can input every variable they find important in their process and let machine learning do the work. Our machine learning doesn’t execute trades automatically, so the PM still has full oversight into any decisions to be made based on the insights AI offers.

- Allowing them to test hypotheses quickly and easily. A PM might think that, say, P/E ratios only over a certain number are important. They can use AI to quickly test that hypothesis by using the vast amount of data our software offers to compare large swaths of different equities (in North America, Europe and APAC region).

ESG Portfolios

ESG inflows continue to hit record highs. Assets under management in sustainable funds hit nearly $1.7 trillion in Q4 2020. Portfolio managers will have to offer not only ESG compliant funds, but, to succeed in a crowded marketplace, performant ones as well. Fund managers may come across problems in ESG investing, like portfolios that are too heavily weighted towards technology (not having adequate diversification), finding the right balance of sustainability and profit, and ensuring that ESG is more than just hype. We found that combining ESG and AI can lead to better results for managers than simply utilizing ESG alone. Read more in our white paper.

Machine Learning Overlays

Some institutional investors worry that using AI in finance means high turnover and unfamiliar or untradeable positions. We have created many ways to fine tune an investment portfolio to control for turnover, blacklist certain stocks, set minimum market caps, and allow portfolio managers to stay within their fund’s particular constraints.

One of the ways our clients have begun implementing AI in their process is by applying a machine learning overlay to their existing portfolio. We go into more detail in our white paper, but basically, we were able to add an average of 232 bps of alpha to different funds, without adding or removing a single name from the manager’s original portfolio. Through using ML to alter position sizing (up when the machine likes a stock, down when it doesn’t), those small changes added big results.

Takeaways

These are just some of the ways fundamental institutional investors are finding results with AI today. Using AI or ML in your process can be additive and simple (of course, we are always happy to discuss full quant strategies too!). Artificial intelligence is simply another tool in the portfolio manager’s arsenal, like Excel or Bloomberg. If you’re curious to learn more, reach out to us here – we love talking about AI and finance!