Executive Summary

- Factor timing is a very predictive use of machine learning for investment managers

- Utilizing factor timing can help flag signals on momentum, value, volatility and other factors

- Our machine learning surfaced the switch to Value over Momentum in early 2021

- Capital markets expertise is still needed to glean the most value from the insights artificial intelligence can provide

We recently discussed how investment managers might want to use artificial intelligence and machine learning to perform factor timing. In that blog post, we showed that using AI and ML for factor timing led to average returns of +1.42% in momentum factors, +5.39% in volatility factors and +2.22% in size factors. As value stocks make their resurgence, in what the Head of SPDR Americas Research says is the “largest monthly excess return over growth stocks in February (9% and a two standard deviation event) since 2008.”, we thought it would be a good time to revisit how implementing artificial intelligence and machine learning to time factors can help institutional investors.

How Boosted.ai factor timing works

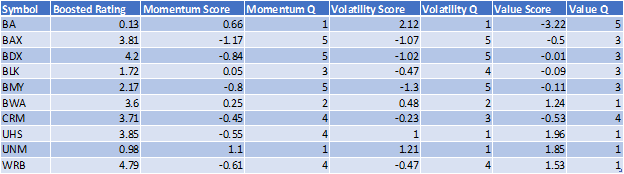

Our factor timing works by using our machine learning to analyze data in order to generate a rating for every stock in the universe (5 stars means the AI predicts a stock will do well, 1 or 0 stars means the AI predicts it will do poorly). Meanwhile, we can also rank every stock in the universe by its factor score.

For example, stocks that have gone up the most will end up in the top quantile of the Momentum factor. The same process can be applied to every factor score (like Value, Volatility, etc). Below is an illustration of how the process works, showing a selection of S&P 500 stocks and some of their factor scores / quantiles along with their Boosted.ai rating.

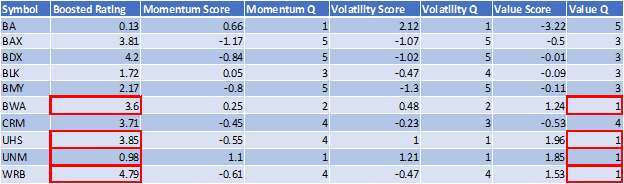

To determine a score for Value Q1, we look at all the stocks that are in Value Q1 at that moment in time, and what their Boosted.ai rating is. In the below example, BWA, UHS, UNM, and WRB make up Value Q1 with an average score of 3.3 (higher is better).

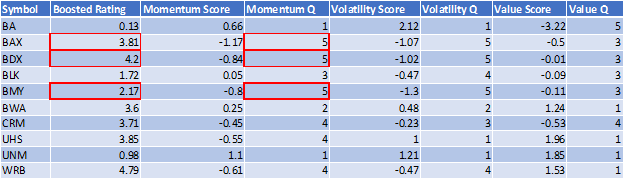

We can compare Value Q1 and its average rating to Momentum Q5 by grabbing the stocks that make up Momentum Q5 (in this case BAX, BDX, BMY) like so:

The average rating for Momentum Q5 is 3.39. Compared to Value Q1 with an average score of 3.31, we see that currently the machine (very slightly) prefers the least momentum-y stocks to the most value-y stocks.

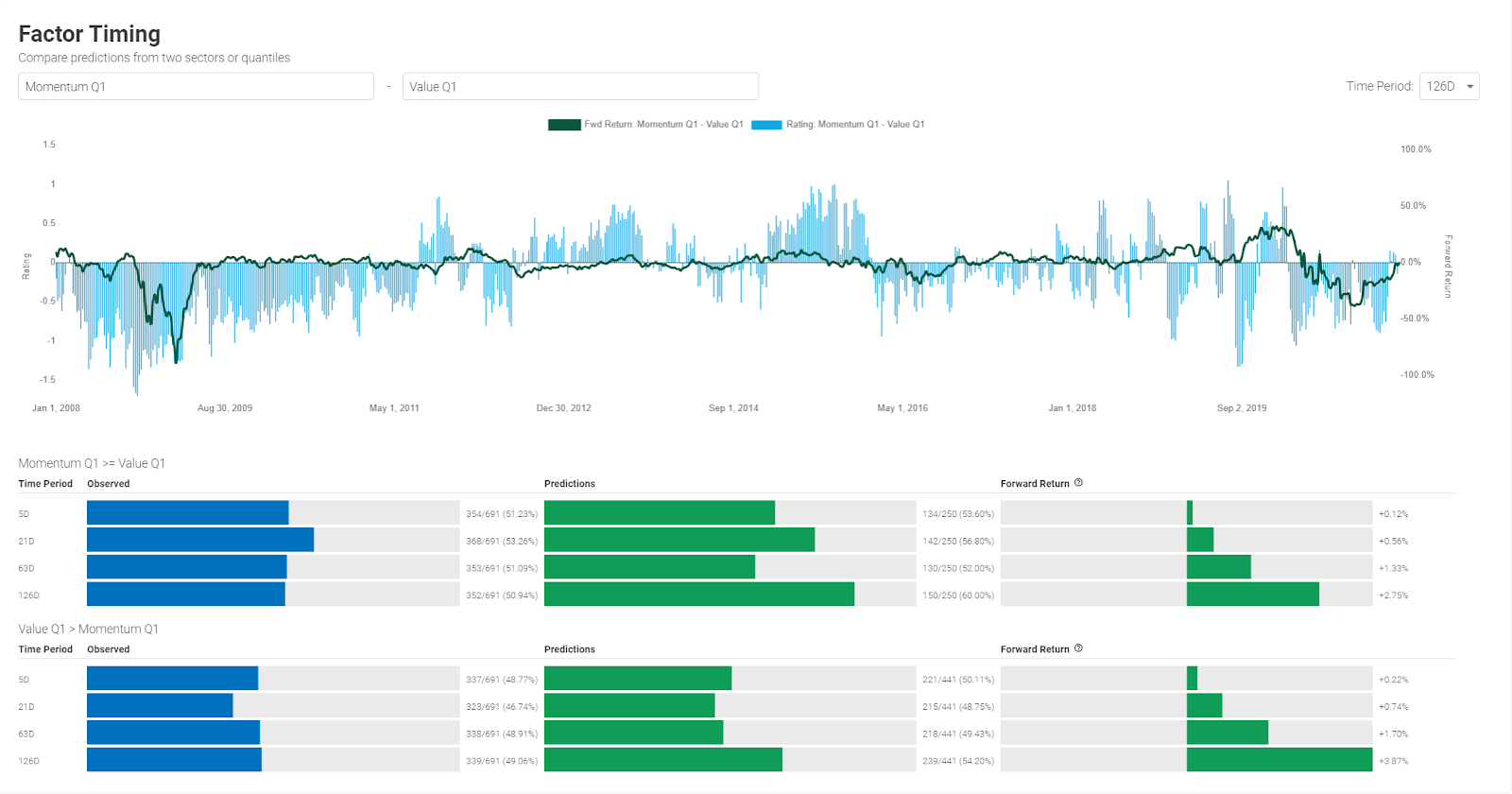

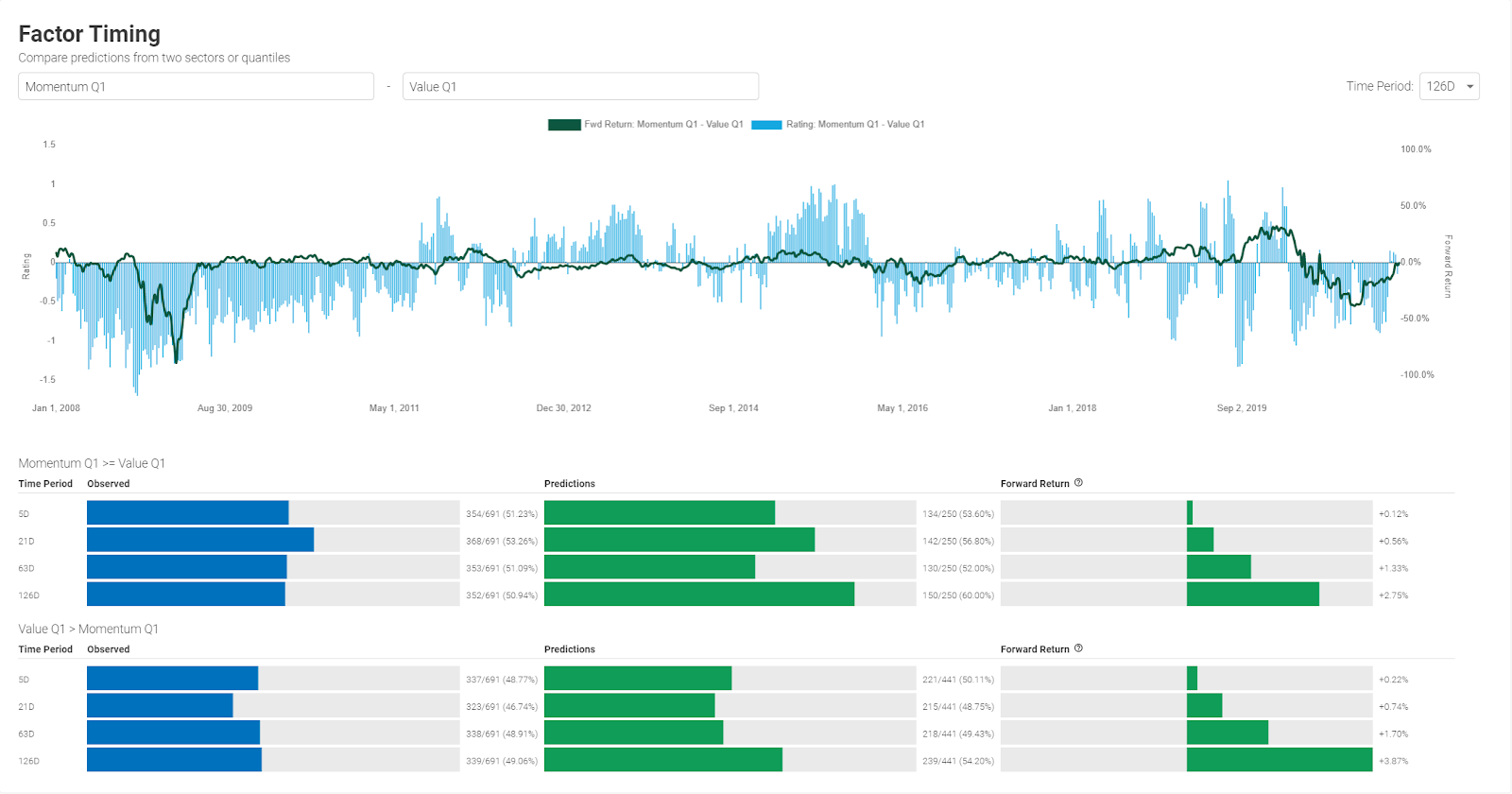

How to put factor timing to work in your portfolio

Through our Factor Timing we can now automate this analysis across any factor quantile or sector you wish. In the below example we can make a more intuitive comparison – Momentum Q1 vs Value Q1. That is, comparing the ratings for the stocks with the highest Momentum vs the stocks the most Value. When the blue bars are above the X Axis it means the machine preferred Momentum and when they are below it preferred Value. The green line is depicting the 6 month forward return of those Momentum stocks minus those Value stocks. So a good result is the blue bars being above 0 at the same time the green line is above zero (or vice versa).

This shows that our machine learning does an excellent job of deciding when to go long Momentum or long Value, improving the accuracy of all such predictions and generating a positive return across multiple time frames when it makes those recommendations.

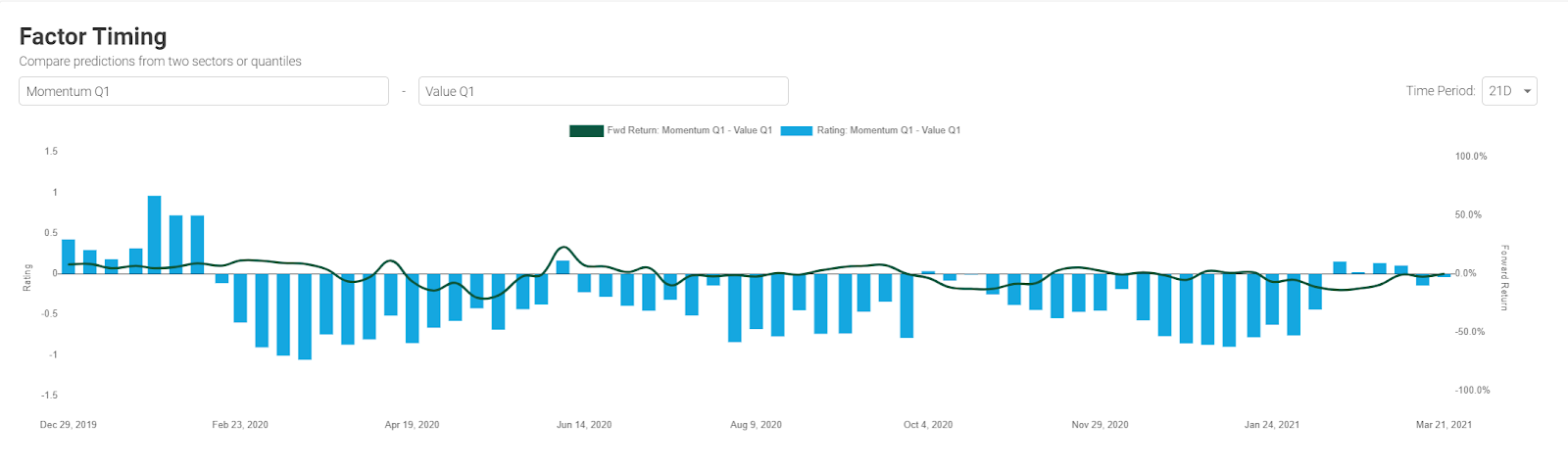

A natural follow-up question might be “That’s interesting, but how would this have helped my portfolio during the uncertainty of 2020?”.

The above chart shows the recommendations just for 2020 to present versus the forward one month return. You can see that our machine learning switched to preferring Value over Momentum a little bit early (February 2021) and stuck pretty strongly to Value for the remainder of the periods.

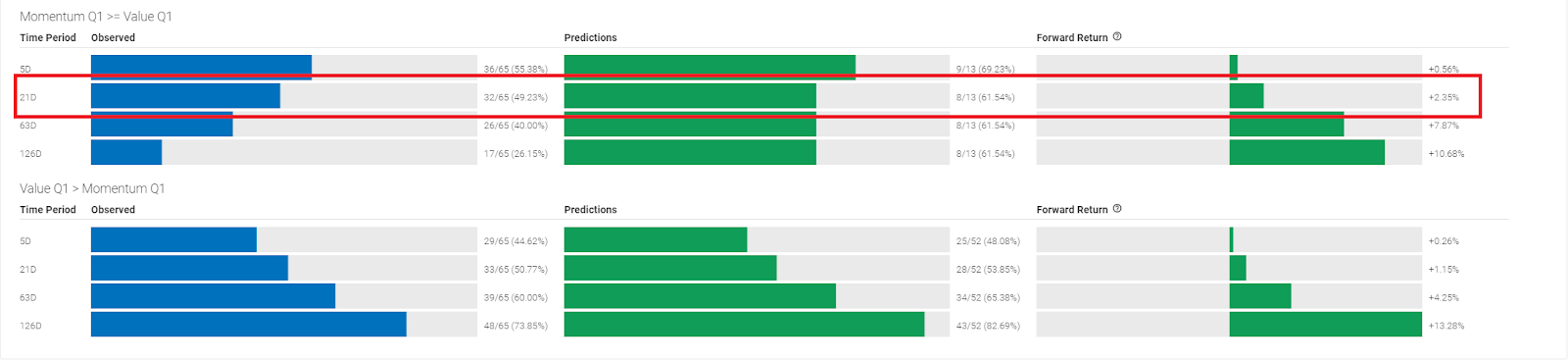

You can also see how much accuracy and performance was helped by listening to the machine. For example, on a 1 month forward basis Momentum Q1 only beat Value Q1 49% of the time – but following the machine’s recommendations you were correct 61% of the time and a manager could have made an average of 2.35% for following that advice.

Factor timing benefits from your capital markets expertise

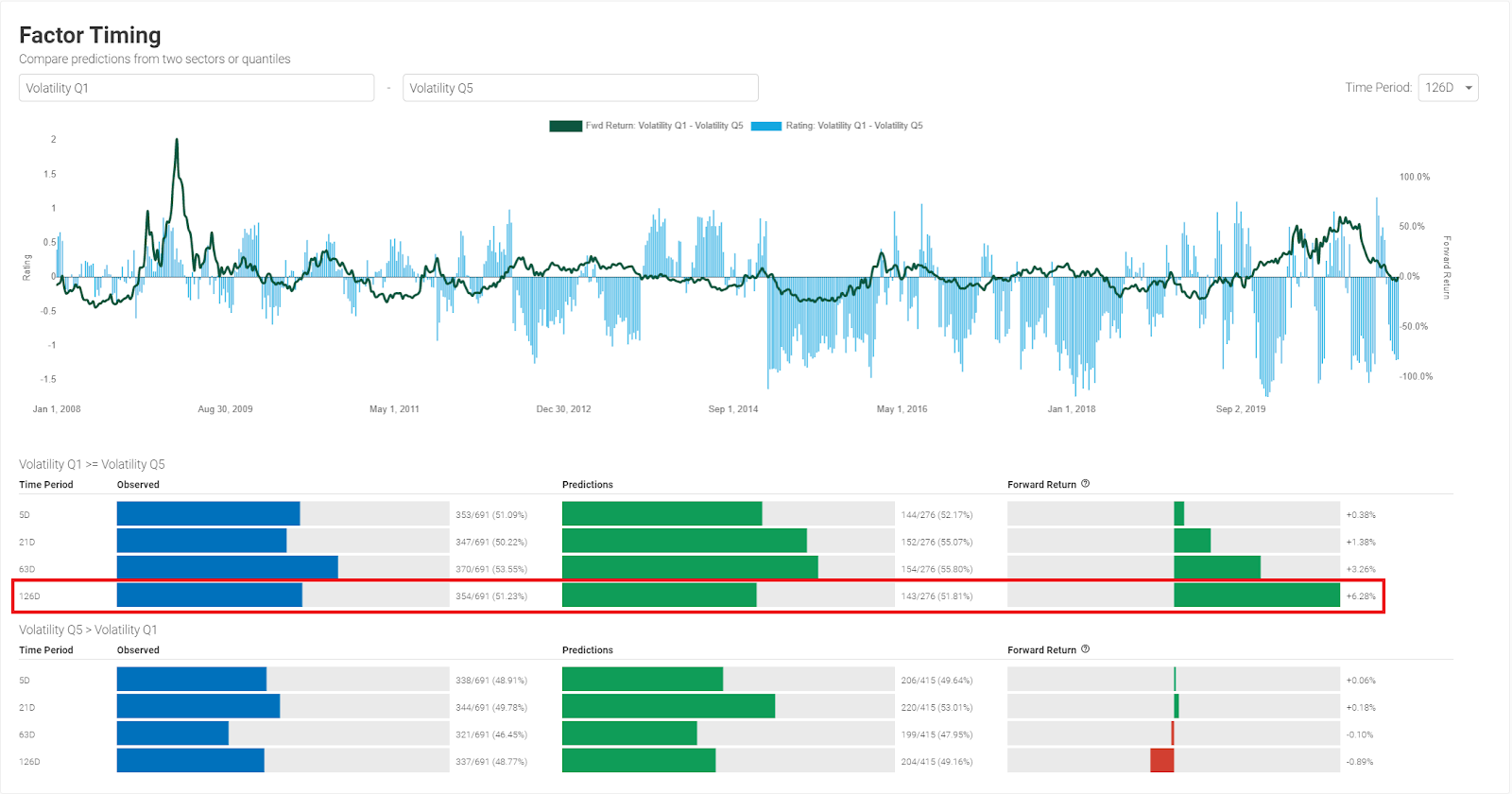

Sometimes the information that comes out of factor timing can be a little bit more nuanced and harder to understand. For example, in the chart below you can see that our machine learning strongly preferred low volatility stocks (Volatility Q5). It prefers Volatility Q5 in a 2:1 ratio over Volatility Q1 (the most volatile stocks). And as a result, the “signal” for going long low volatility stocks isn’t materially more accurate than random guessing and there is no positive return associated with it.

However, when you look just at the much more rare “buy volatile stocks” signal you can see that while also not being materially more accurate than observations – it was hugely more performant. You made almost 6.3% every 6 months (on average) by going long the most volatile stocks and shorting the least volatile stocks when the machine recommended it.

The ability to generate and then interpret all of this data showcases why we feel so strongly about quantamental investing, where human PM plus machine learning combine to become greater than the sum of their parts. Factor timing is another arrow in an investment manager’s quiver – another way to add value to their portfolios. As investors demand more from their investments, being able to use every tool at their disposal will become even more crucial for PMs. Combining all types of big data and being able to interpret its meaning will be the way of the future for all asset management.