What investment manager wouldn’t love a crystal ball? Something to warn them when black swan events like Covid-19 hit, and one that can alert them when things like GME or vaccine news can shift the market. Harnessing the power of artificial intelligence is not a magic wand, but making efficient use of the vast swaths of data available can help make investment managers feel a bit more prophetic.

Take January 2022 – asset managers running long / short strategies have taken a large hit. If they had used AI and machine learning to optimize their signals, their drawdowns may have been a bit better this month. Here, we’ll walk through an example of how making use of the predictive power of AI can help asset managers control risk.

In this scenario of 3 Russell 1000 models with identical portfolio construction, but different methods of ranking the securities, we increase performance from -3.95% to +2.07% and +1.97% while significantly reducing volatility. This model and its performance is based on the first two weeks of January 2022.

Non-diversified equity portfolio risks

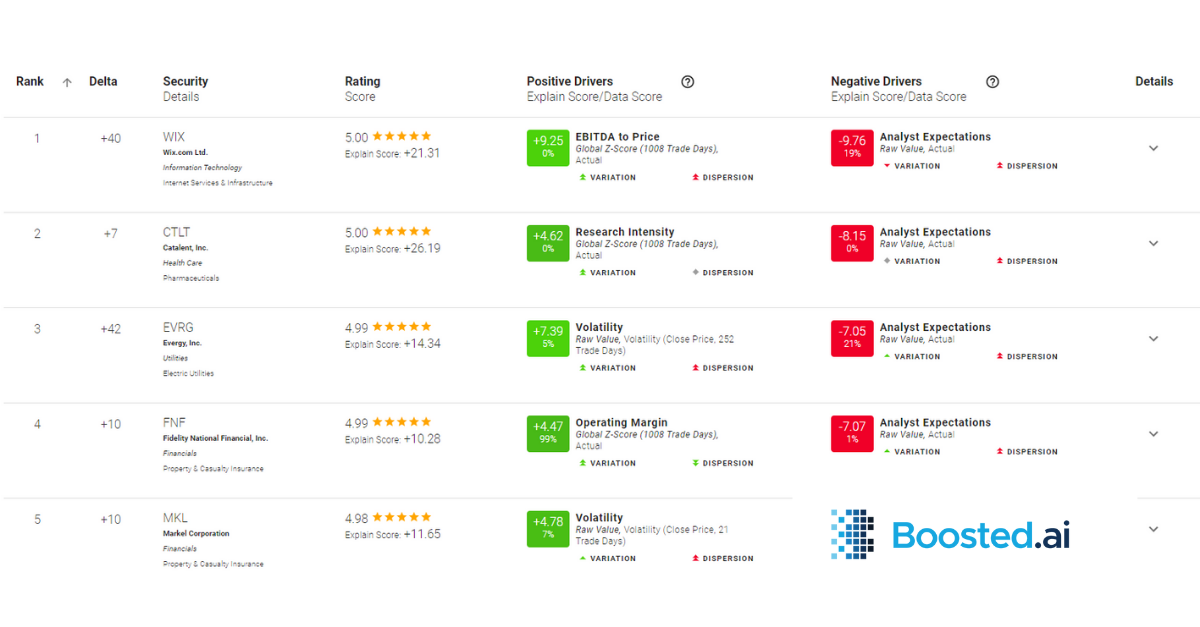

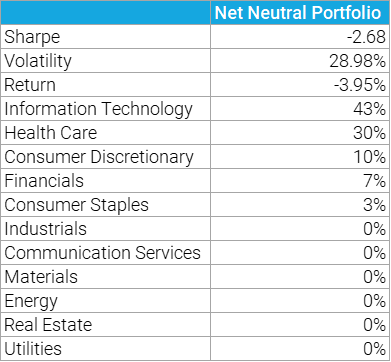

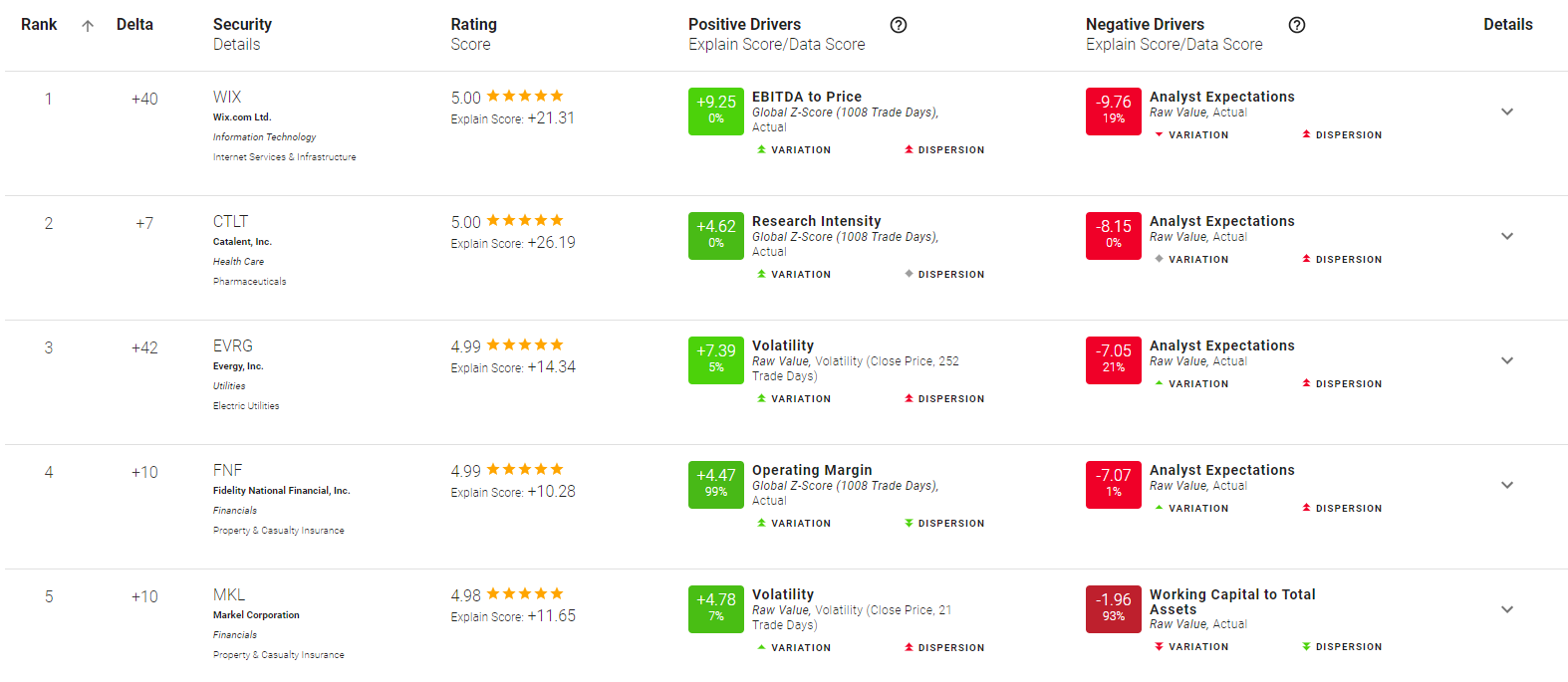

Portfolios with large, concentrated bets in stocks have been hit particularly hard this month. Even some of our machine learning models (like this Net Neutral one highlighted below) – built within Boosted Insights, our machine learning finance platform – sought to make large, concentrated bets in healthcare and tech stocks. We highlight the top 5 picks here and also showcase the sectors it bets most heavily in. The volatility of this portfolio was 28.98% from the beginning of January to January 13 and it is highly concentrated in Information Technology stocks (43% of the top 30 picks).

Our machine learning models, without the benefit of signal optimization (more on that shortly), have ranked these stocks and sectors very highly, as in, ones it thinks will do well this month. Of course, with large, concentrated bets, an investment manager can be very right or very wrong.

Optimizing signals to reduce risk in stock portfolios

Our machine learning works in two ways: first, by distilling the investment manager’s view of what is important in stock picking and applying it to capital markets data (essentially performing top-down or bottom-up fundamental analysis with speed and accuracy) and second, by using portfolio analysis tools to optimize the resulting portfolio for the manager’s needs (say, low turnover or volatility, being market neutral, maximizing alpha, constraining risk factors, etc.). Investment managers seeking to reduce their risk even further can make use of an optimization built into Boosted Insights, called signal optimization.

Our predictive machine learning takes all available data for a bucket of stocks and sorts them into “unnamed” risk factors, ranging from Machine 1 to Machine 10. These are the biggest risk factors in descending order and adaptive – so during March 2020, Machine 1 might have been Coronavirus and stocks like cruise lines and airlines were concentrated within it. We have added functionality to control for those risk factors at the signal level to help diversify the top ranked stocks in our models, so no baskets are over or under exposed to any particular risk. Our ML risk factors are sorted by concentration of similar price action data.

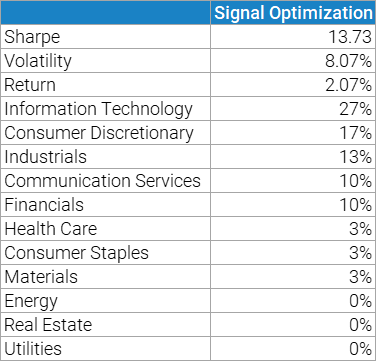

New equity rankings

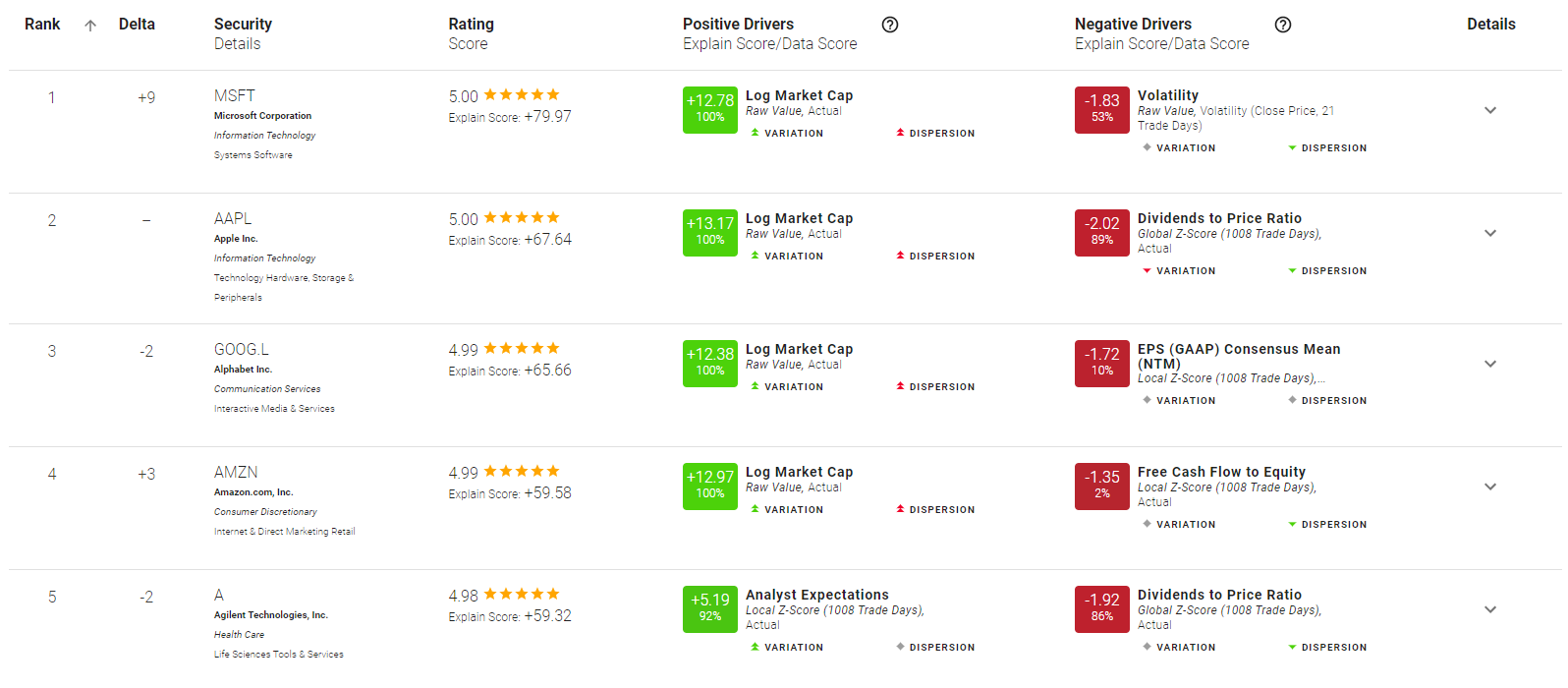

With these optimizers turned on, the rankings change to incorporate the new risk constraints. The result is a more varied portfolio with stocks in different sectors. The below images show this new optimized signal portfolio’s top 5 picks and the new, more diversified sectors of the top 30 long picks.

Utilizing our machine learning stock optimization, which uses big data to effectively isolate when individual stocks are too heavily weighted towards one risk, the resulting portfolio’s top 30 picks are significantly more diverse. The volatility is at 8.07% and the return is positive at 2.07%.

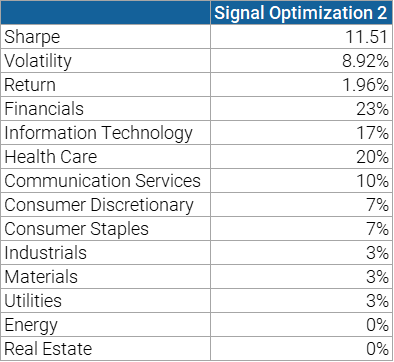

Even further diversification through artificial intelligence

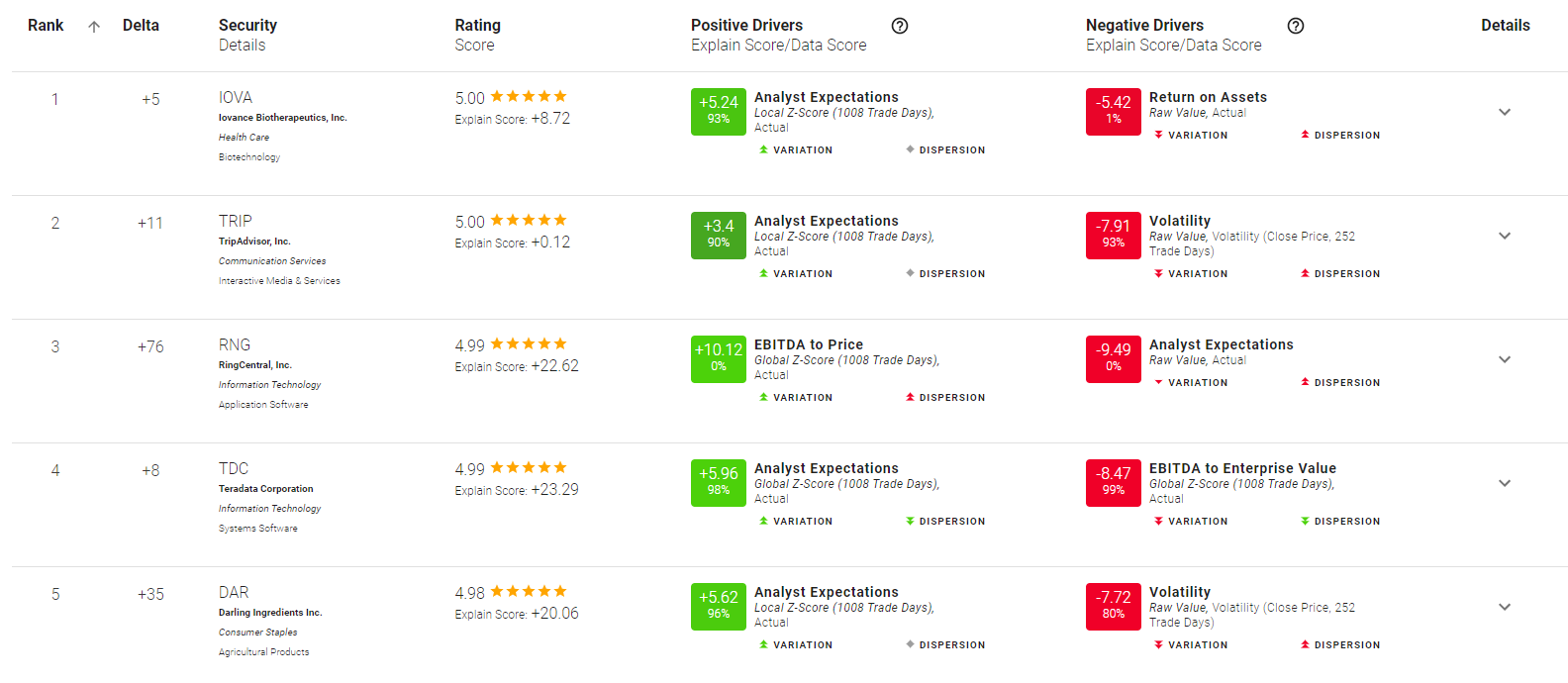

A new enhancement to Boosted Insights is our signal optimization v2. This is a holistic view of risk factors and takes non-pricing data into account (balance sheet, income statement, etc.). This results in new rankings and even more diversified long picks in the top 30 stocks. The results are somewhat similar to our first signal optimized portfolio, but with the benefit of even more stock diversity to control for risk.

Takeaways

Large concentrated bets can work, but if the market ever moves against an investment manager’s strategy, those bets can mean the undoing of their portfolio and, in this case, a tough start to the year of -3.95% in two weeks. Using our machine learning risk factors, we increased performance from -3.95% to +2.07% and +1.97% while significantly reducing volatility and increasing Sharpe.

Making use of data-driven artificial intelligence technology can help reduce risk in manager’s stock rankings prior to entering the portfolio by widening the number of sectors and types of stocks. Signal optimizers, which can identify and then control for varying types of risk, are a good way to use machine learning for this purpose. If you want to know more about how we created these portfolios and how we help institutional investors manage their risk, reach out to us here.