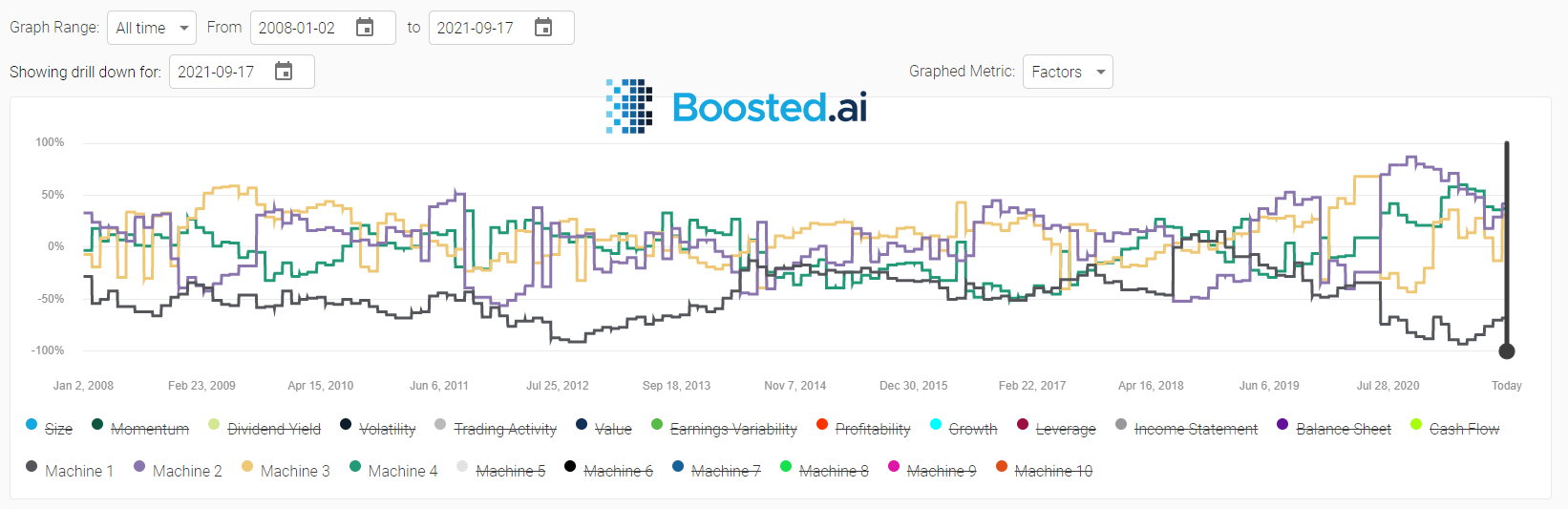

Machine learning for asset management has a lot of moving pieces: portfolio allocation, risk management, and ensuring that any predictions the machine makes are explainable to different stakeholders are just a few things investment managers have to think of when creating their ML portfolio models. Using statistical techniques to summarize and explain complex market movements and interactions through smaller, more compact factors, can help asset managers make sense of the complexity of their ML portfolio models.

A similar approach is used in Risk Mitigation and Portfolio Analytics and in other areas of scientific data analysis. Within our artificial intelligence platform – Boosted Insights – the output of this analysis identifies which stocks are likely to experience stock price shifts (based on what is happening in the world and capital markets) and groups them together. It then groups the results under Machine Learned Factors.

These machine-learned factors are unnamed – Machine 1, Machine 2, Machine 3, and so on. Though we have found these to be useful on their own (especially during unpredictable events like Coronavirus, the GME short blow up, and the quant shock), our aim is always to expand the transparency of our AI. We knew that identifying commonalities within these factors would help institutional investors more fully understand their machine learning portfolio models, so we sought out a unique solution.

Semantic risk factors

To put a name to the machine learned factors, we looked to another aspect of artificial intelligence: Natural Language Processing or NLP. We previously discussed NLP techniques in our post about modelling the Coronavirus risk factor. We used NLP to create “Topic Modeling” to identify those unnamed factors. Within Boosted Insights, we call this “Semantic Risk Factors”.

Our approach on a fundamental level is to create a compatible semantic representation of both stocks and terms – so called descriptors, words and phrases – based on text and data available in the public domain. In more technical terms – putting companies and terms used to describe them into a shared vector space to find commonalities and identify dependencies.

With this representation we are able to map the information about distribution of stocks in each factor to a small set of descriptive terms that characterize this factor.

Putting NLP to work for investment management

What does this look like and how can it be used in practice?

To start, we are able to identify groups of stocks that move together and then further identify how much volatility these groups of stocks account for and which groups move in the opposite directions.

For example – as shown below, Machine 1 indicates that Cruise Lines, Airlines, and Oil & Gas stocks have been moving together, and generally in opposite directions from stocks related to Computing and Medical Devices and Video Games. This factor accounted for 64% of volatility.

A lot of the optimizations are already made automatically to mitigate risk via portfolio allocation given these results, but users can manually set the filters for these factors, and know what they are controlling for.

Next, we dive deeper and showcase exactly which securities fall into these groups:

We showcase how much volatility in the stock universe is explained by specific equities, their portfolio exposure and average machine stock rating and its change. This allows users to understand how the portfolio allocation algorithm is working to balance risk and reward within their machine learning portfolio models, given the volatility.

Lastly, we break down the universe into the classic GICS sectors to showcase their market volatility and corresponding portfolio allocations:

Using this view, users can optimize sector choices and further customize portfolios through filters to balance risk and ratings to suit their investment style.

Takeaways

Deeper understanding and transparency within our machine learning platform is one of our main goals here at Boosted.ai. Semantic risk factors is another step towards a more explainable AI, but also helps asset managers identify which sectors or individual stocks are grouped together in different risk factors. By arming investment managers with as much knowledge and clarity into their ML models as possible, we know that their capital markets expertise can drive success for their portfolios. To see a demo of this feature or for any other questions, please reach out to us here.