Here at Boosted.ai, we speak to a variety of potential users of our artificial intelligence investment management software and many traditional investor’s first statement is something along the lines of “Sure, artificial intelligence is interesting, but how would I use it?”. It is a topic we covered that in a previous post, but to recap, some use cases are using the power of AI to generate data-driven ideas for your portfolio, machine learning powered risk mitigation, and creating targeted baskets. We believe all asset managers can benefit from utilising artificial intelligence and machine learning in their process.

After a person is interested in harnessing AI to empower their stock picking, the next question is something like “I have to build a model? Why? And how?” Here, we’ll walk through some early tips to building the most robust machine learning models for your investment management needs.

What is a model?

Artificial intelligence (and its subset, machine learning) is powered by models. Broadly, a model is the set of parameters someone uses to allow machine learning to do its work. As Microsoft defines it, “a machine learning model is a file that has been trained to recognize certain types of patterns. You train a model over a set of data, providing it an algorithm that it can use to reason over and learn from those data.”

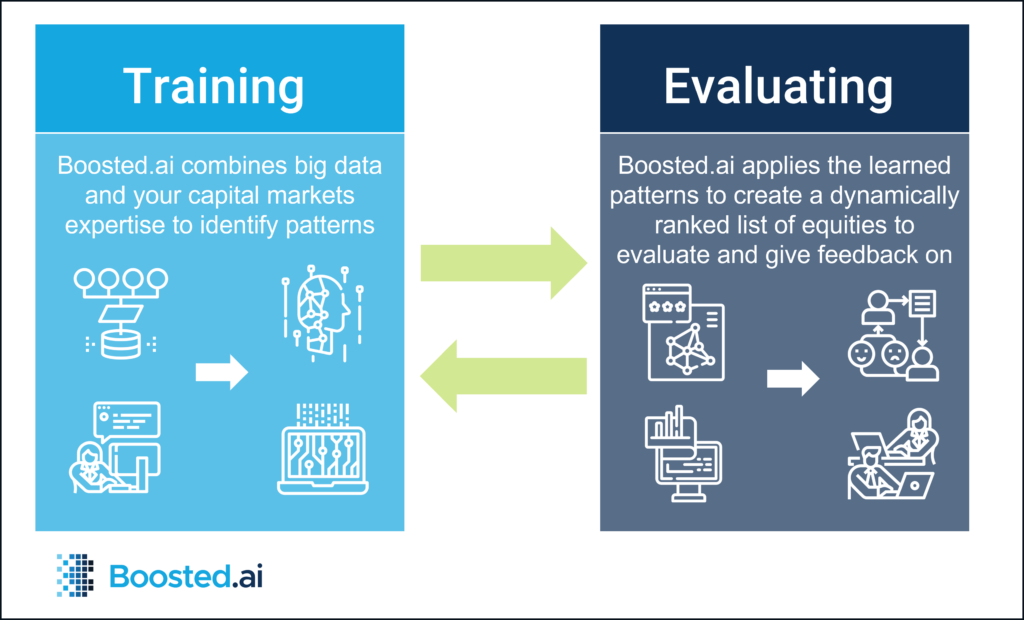

Within our platform – Boosted Insights – that means a model is the set of rules and data the user finds important in stock picking. Things like their investment universe, goals (alpha or pure return), which features they use to pick stocks (i.e. P/E ratio, EPS, or more technical ones like Bollinger bands) and portfolio settings (how they want the model to trade) all go into a Boosted Insights model. After the model has “trained” (learned from the inputs provided), a client can begin evaluating it. Like many things, building and perfecting AI models takes a bit of skill and a bit of practice. At Boosted.ai, it is an iterative process, one where customer success and the investment manager work together to create a model that works for their needs.

AI Investment Management Tips

Tip 1: Ensure the backtest is long enough

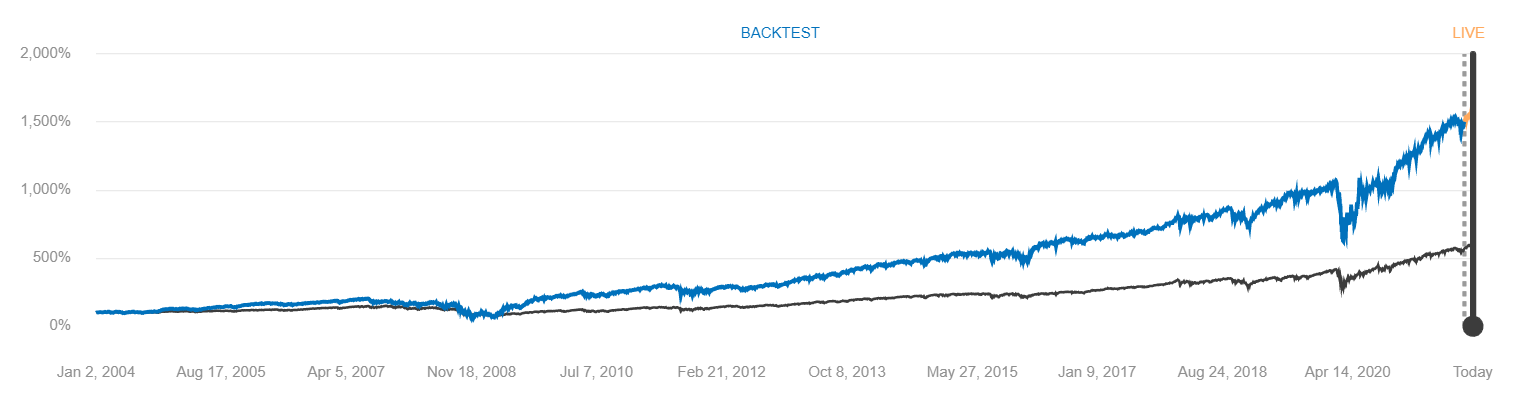

The enemy of many artificial intelligence models, especially for asset management, is not enough data. Capital markets data can be very noisy and we are in the midst of a prolonged period of growth (with some black swan events like Covid-19 thrown in for good measure).

A 1 year backtest that is great might hide weakness the model has in other years (i.e. outperformance in a 2015 environment but not in 2016). A longer backtest gives you the opportunity to see how it does across more regimes and understand how it will perform in adverse conditions (i.e. 2008, 2011, 2019, 2021). Long Term Capital Management, once one of the most successful hedge funds in the world, collapsed in part because of models that only went back 5 years. We recommend at least 10 years in a backtest. Within Boosted Insights, we are training / validating in an out of sample 8 year window and then back testing that trained model on a subsequent period of data.

Tip 2: Your model is only as good as its data

Like the point above about having enough backtest years, a model with corrupted data will learn false lessons. For example, if a dataset only includes existing companies within a universe (like the S&P 500 or the Russell 1000), the machine might learn that all of those companies are stronger than they are. by not including the companies that fell out of the S&P 500 the machine cannot learn what failure looks like – so it will be biased to think that any downturn in a stock is a buying opportunity. At Boosted.ai, all of our datasets have been cleansed by our data scientists. Our algorithms even flag when something in a dataset a client uploads looks awry.

Tip 3: Sometimes, less is more

A natural inclination some asset managers may have is “why don’t I just use every single variable possible and let the machine decide?”. It makes sense theoretically – throw as much data at the machine as possible and you will get the best result. In practice, however, it doesn’t always work that way.

At the highest level, our machine learning algorithms focus on using data to split the universe into winners and losers. Giving the machine access to too much information can create overfitting and find spurious correlations (i.e. it was Tuesday and it was raining and the market went up, therefore buy the market when it rains on Tuesdays). Using targeted data points that make intuitive sense to the user (i.e. P/E ratios or earnings growth) is more likely to result in a robust, generalized model.

Tip 4: Set clear goals and know what success looks like

Another question we frequently hear from institutional investors is “which is the best algorithm to use?”. We have proprietary, finance-specific algorithms here at Boosted.ai that account for the difficulty within capital markets prediction (more on that here), but another way to look at this question is that in order to determine the best algorithm to use, the first step is for the investment manager to understand what problem they are trying to solve.

Every asset manager would like better everything – return, alpha, Sharpe ratio, etc. – but the clients we have that have seen the most success using Boosted Insights have a clear idea of their goals. For example, a person who knows their turnover must be under 200% per year, return has to be in step with benchmark returns, and they seek to keep volatility under 30% has clear, identifiable goals that our customer success representatives can help them work toward.

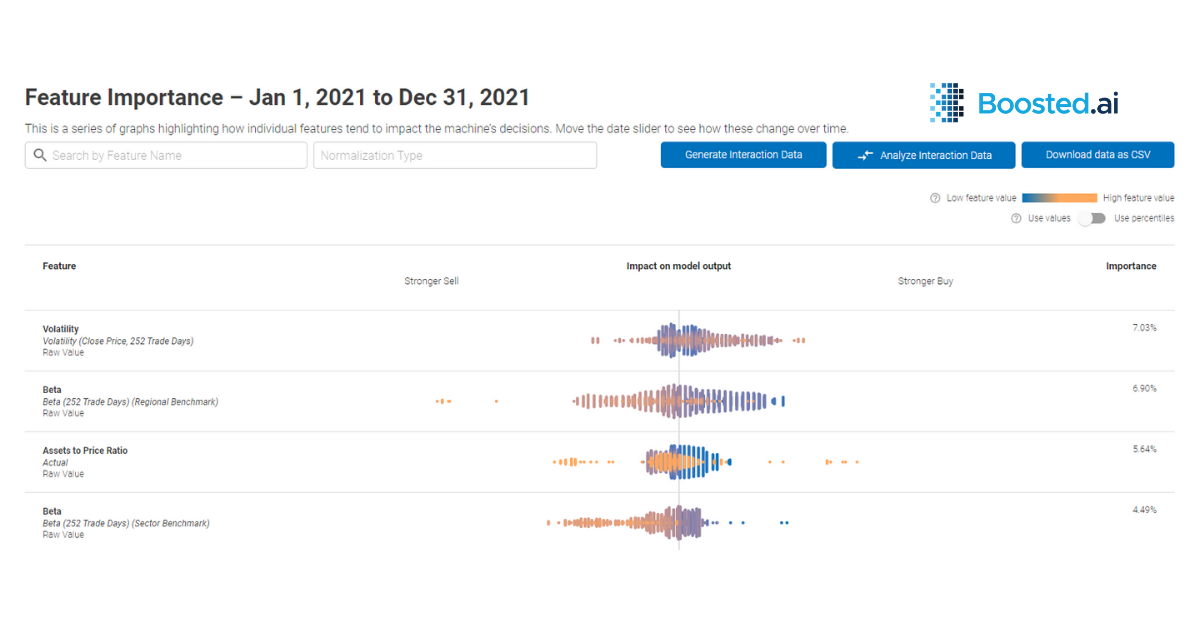

Tip 5: Explainability is everything

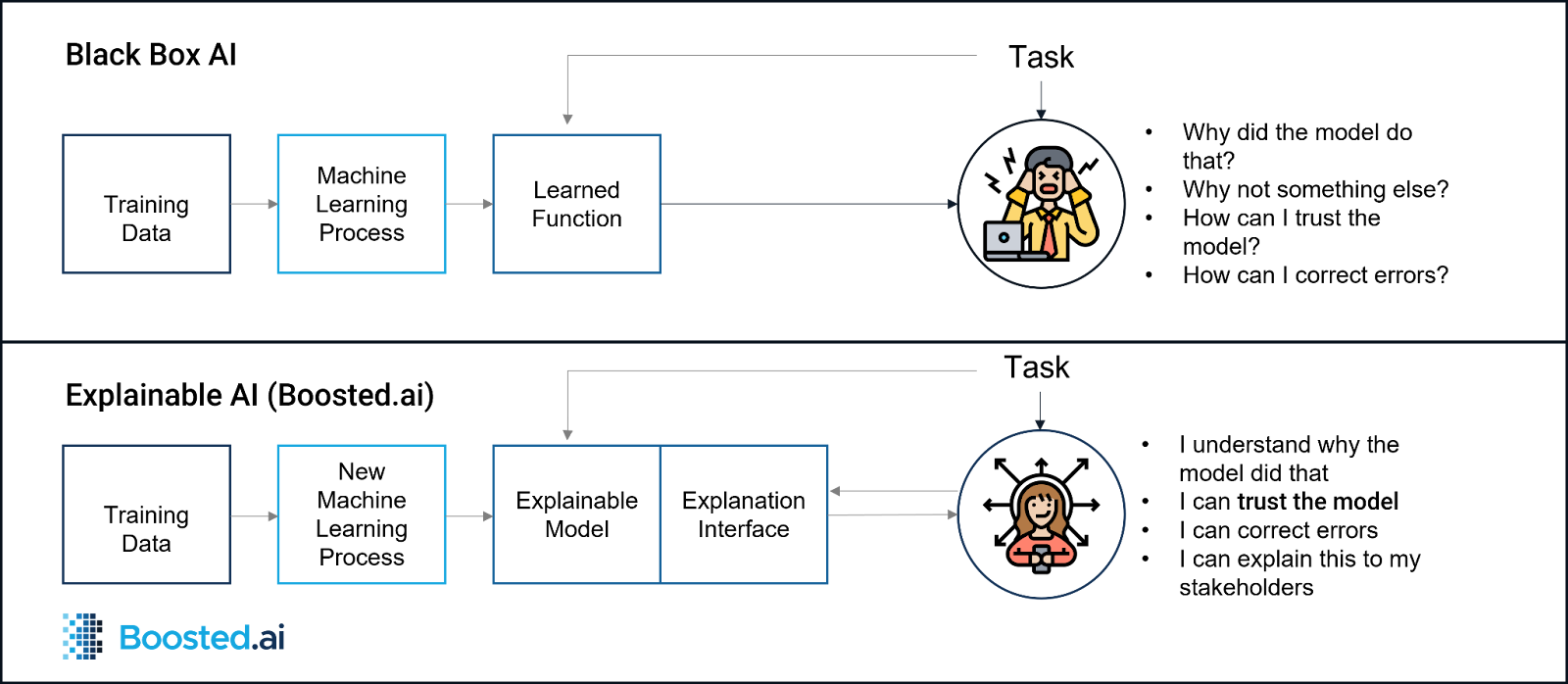

Results are important, but difficult to sell to stakeholders if an investment manager can’t explain the model and its decisions. Many machine learning apps can be “black box” in nature, meaning that why the machine made any decisions are not understood by the end user.

In order to trust their systems, investment managers need explainable AI for their models. Boosted.ai is constantly seeking to update our explainability engine to provide more glass box, less black box artificial intelligence. An additional benefit of explainable AI for asset managers new to creating models is that understanding the inputs and their interactions helps build trust that a model will work (or can be tweaked to work).

Takeaways

Building models through machine learning is an iterative process. An asset manager probably won’t think “okay, finished!” after the very first investment management model they create. Working with a team of experts, both within capital markets and data science, can help fund managers get there faster. It also helps to have clearly defined goals and success metrics in place, both to understand what “winning” looks like, and to know how to tweak and iterate on their ML models. If you are curious about implementing AI within your investment management process, please reach out to us!